By Cameron Williams, Director of Research, SVN International Corp.

The industrial real estate sector is a dynamic asset class undergoing a multitude of transformative changes. By 2025, online retail is projected to account for a quarter of total purchases, driving the rise of direct-to-consumer (DTC) brands and the demand for expedited shipping. This has prompted smaller brands to spur the development of shared logistics facilities, offering warehousing and logistical services to meet this growing need.

By Cameron Williams, Director of Research, SVN International Corp.

Downtown office vacancies continue to climb, with a significant portion of the workforce operating remotely. The trend away from traditional office usage is reflected in a projection that office conversion projects are expected to more than double, driven by incentives from state and local governments.

This shift comes as the conventional five-day office workweek is rendered obsolete, prompting a search for alternative uses for empty office spaces. While the White House has proposed a $35 billion initiative to transform these underutilized spaces into residential housing, aiming to create over 170,000 units, the question remains whether this approach is viable.

Beyond residential conversion, innovative uses for this space are being considered, from multifamily housing to vertical farming and medical/life science facilities, as we rethink how best to utilize the evolving urban fabric.

By Cameron Williams, Director of Research, SVN International Corp.

Concluding our energy series is a look into the mineral that is the driving force behind so much new development throughout the country, lithium. Fueled by government incentives and a strategic move towards energy independence, the commercial real estate landscape in lithium-rich areas of the country is bound to be reshaped. One of the most crucial elements in EV and energy storage batteries, regions harboring substantial reserves are attracting considerable interest and are bound to spur demand for industrial spaces for processing facilities, as well as residential and infrastructural development to support the growing workforce akin to historical resource-based boom towns.

By Cameron Williams, Director of Research, SVN International Corp.

An abundance of industrial development is being driven by the burgeoning battery production sector where over the last decade a surge in demand for energy storage solutions has emerged. Beyond EV battery production, these facilities are focusing on battery cells that are meant for storing energy produced by wind, solar, and water. As North America’s battery manufacturing capacity is projected to increase nearly twentyfold by 2030, the ripple effects are palpable in the commercial real estate market, with industrial spaces being rapidly repurposed to accommodate the needs of this high-growth sector. This transformation signifies not just a technological revolution but a pivotal economic shift, as the U.S. positions itself at the forefront of the global energy transition.

By Cameron Williams, Director of Research, SVN International Corp.

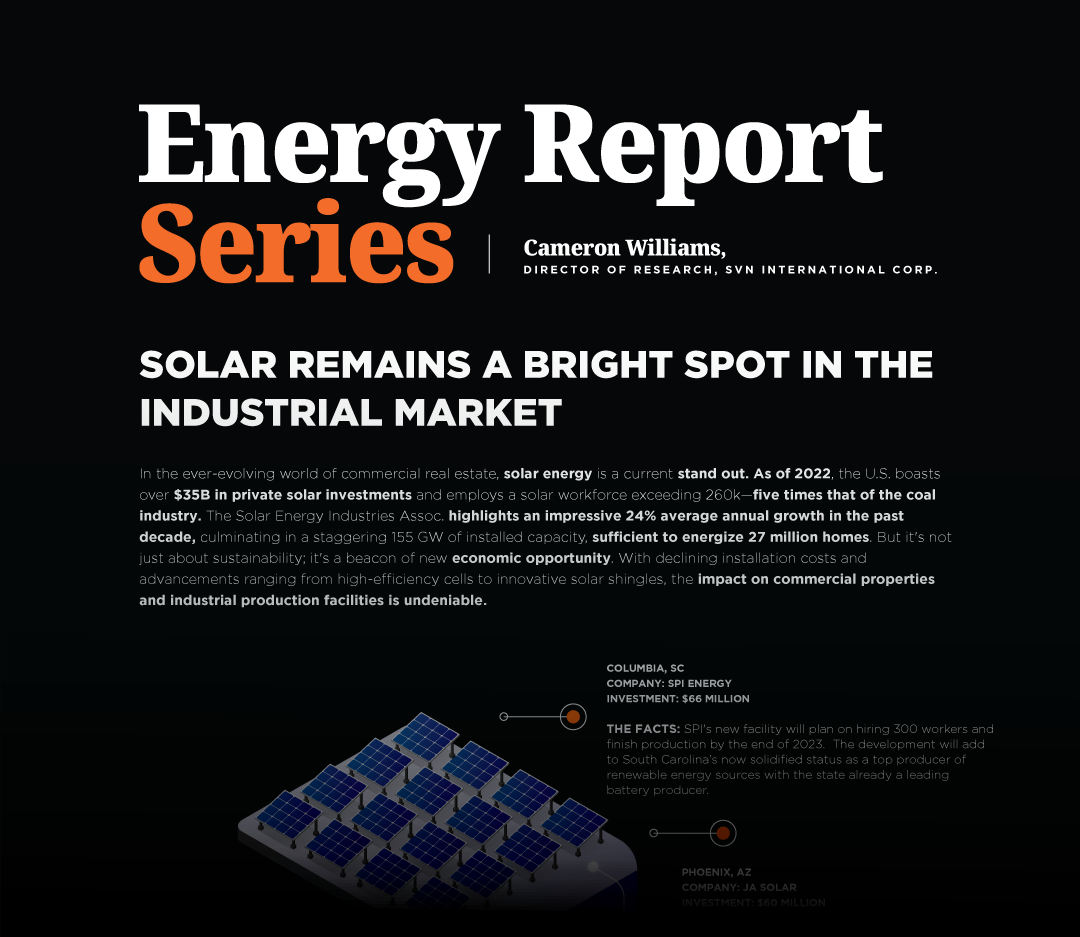

In the ever-evolving world of commercial real estate, solar energy is a current stand out.As of 2022, the U.S. boasts over $35B in private solar investments and employs a solar workforce exceeding 260k — five times that of the coal industry. The Solar Energy Industries Assoc. highlights an impressive 24% average annual growth in the past decade, culminating in a staggering 155 GW of installed capacity, sufficient to energize 27 million homes. But it’s not just about sustainability; it’s a beacon of new economic opportunity. With declining installation costs and advancements ranging from high-efficiency cells to innovative solar shingles, the impact on commercial properties and industrial production facilities is undeniable.

By Cameron Williams, Director of Research, SVN International Corp.

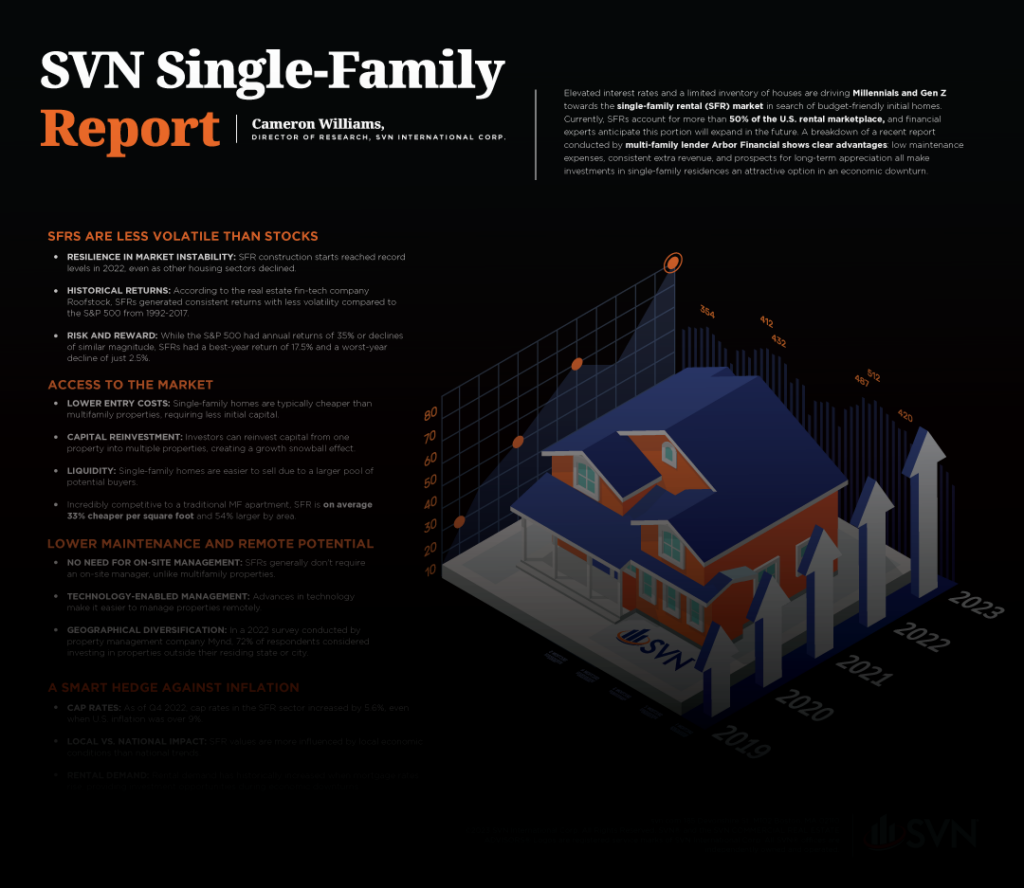

Elevated interest rates and a limited inventory of houses are driving Millennials and Gen Z towards the single-family rental (SFR) market in search of budget-friendly initial homes. Currently, SFRs account for more than 50% of the U.S. rental marketplace, and financial experts anticipate this portion will expand in the future.

An analysis of a recent report conducted by Arbor Financial, a multi-family lender, highlights compelling advantages: minimal maintenance costs, steady additional income, and the potential for long-term appreciation. These factors make investments in single-family residences a highly appealing option in times of economic downturn.

By Cameron Williams, Director of Research, SVN International Corp.

The shopping mall, once considered the pinnacle of consumerism, has been a much-maligned retail class over the past decade. In a 2017 Credit Suisse report, it was predicted that 1 in 4 malls would be closed by 2022. Ironic that most malls have outlasted that bank. While iconic mall-based retailers like The Sharper Image and KB Toys are long gone, the American mall is far from dead. In a recent study conducted by Coresight Research it was reported that shopping malls, especially high-end malls, are experiencing positive growth across nearly all key performance indicators and that with omni-channel sales strategies on the rise these trends are expected to continue into the future.

By Cameron Williams, Director of Research, SVN International Corp.

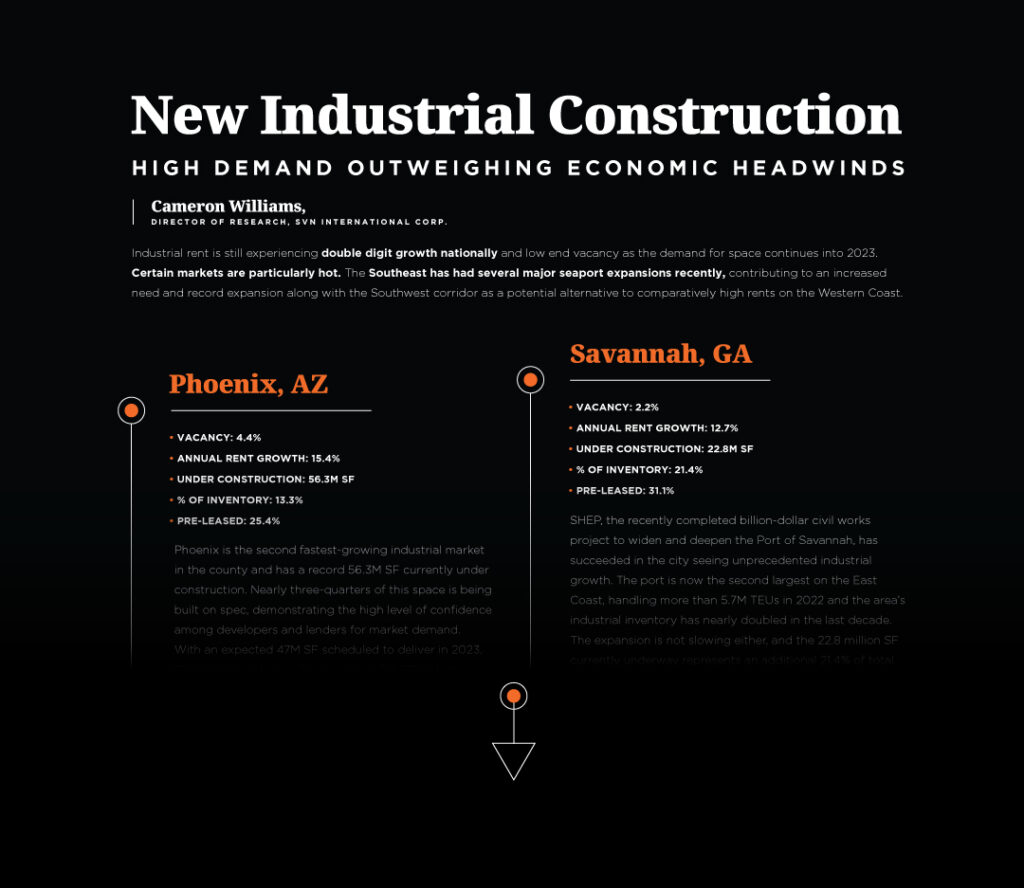

Industrial rent is still experiencing double digit growth nationally and low end vacancy as the demand for space continues into 2023. Certain markets are particularly hot. The Southeast has had several major seaport expansions recently, contributing to an increased need and record expansion along with the Southwest corridor as a potential alternative to comparatively high rents on the Western Coast.

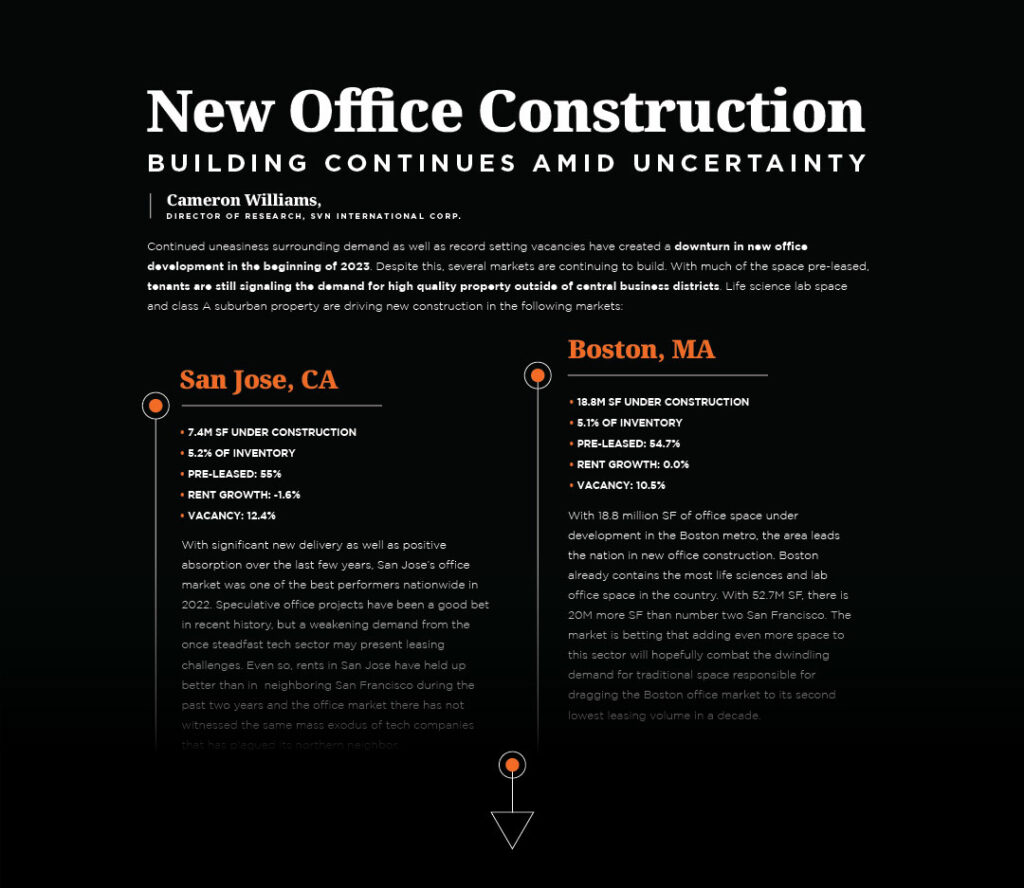

By Cameron Williams, Director of Research, SVN International Corp.

Continued uneasiness surrounding demand as well as record setting vacancies have created a downturn in new office development in the beginning of 2023. Despite this, several markets are continuing to build.

With much of the space pre-leased, tenants are still signaling the demand for high quality property outside of central business districts. Life science lab spaceand class A suburban property are driving new construction in the following markets:

By Cameron Williams, Director of Research, SVN International Corp.

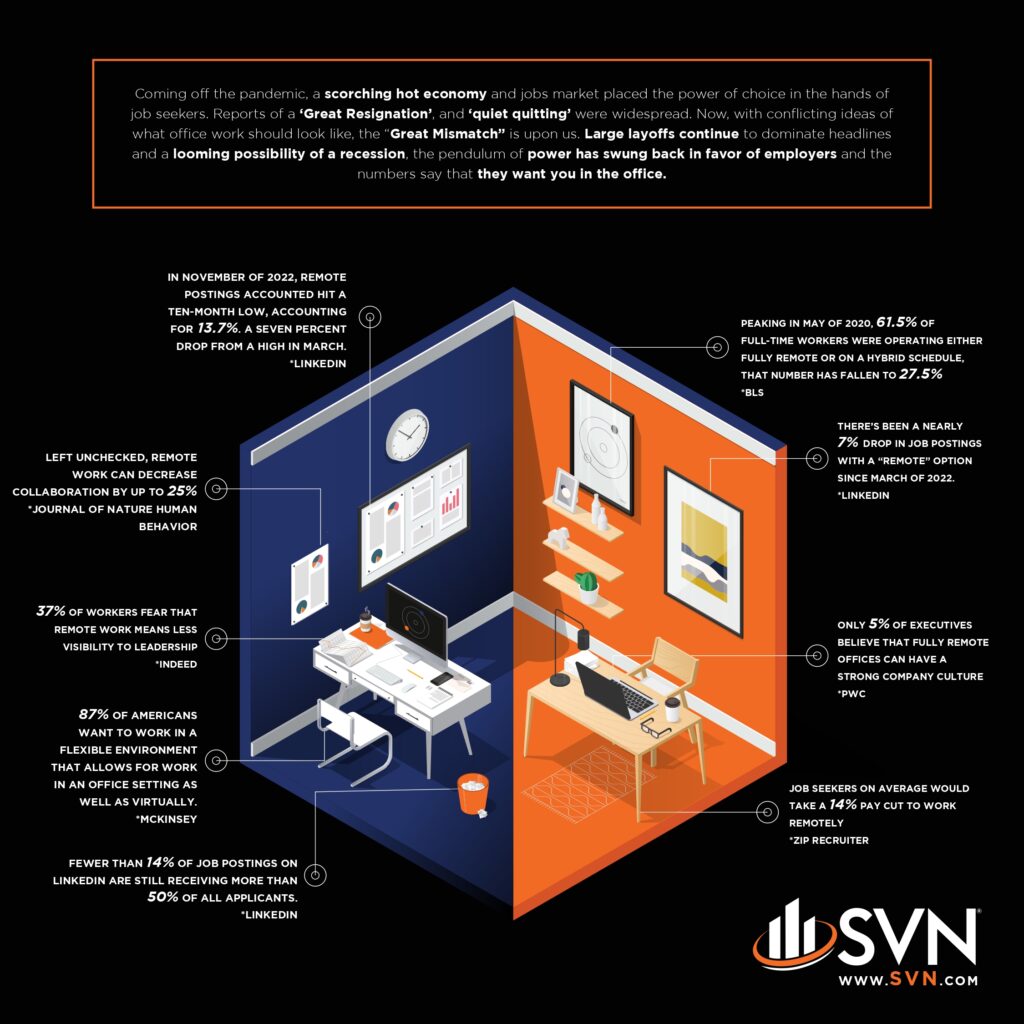

Coming off the pandemic, a scorching hot economy and jobs market placed the power of choice in the hands of job seekers. Reports of a ‘Great Resignation’, and ‘quiet quitting’ were widespread. Now, with conflicting ideas of what office work should look like, the ‘Great Mismatch’ is upon us. Large layoffs continue to dominate headlines and a looming possibility of a recession, the pendulum of power has swung back in favor of employers and the numbers say that they want you in the office.

By Cameron Williams, Director of Research, SVN International Corp.

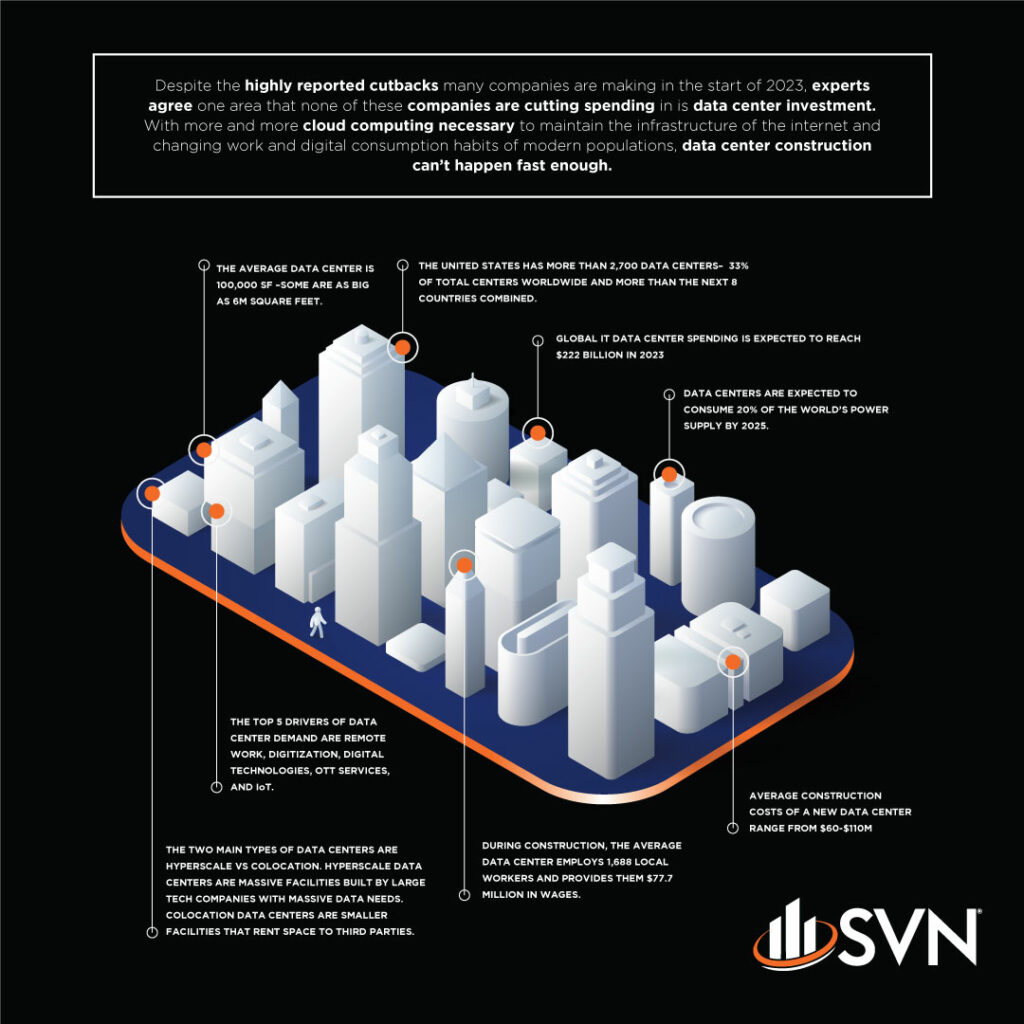

Despite the highly reported cutbacks many companies are making in the start of 2023, experts agree one area that none of these companies are cutting spending in is data center investment. With more and more cloud computing necessary to maintain the infrastructure of the internet and changing work and digital consumption habits of modern populations, data center construction can’t happen fast enough.

By Cameron Williams, Director of Research, SVN International Corp.

In 2022, brick-and-mortar retailers faced challenges such as a looming recession and record inflation, which greatly affected consumer confidence. Despite these challenges, a particular type of retailer will be set up to thrive and there are still plenty of opportunities for success in the retail industry. As the economy improves and consumers become more optimistic, the brands outlined in SVN’s latest whitepaper are well-positioned for success in 2023.

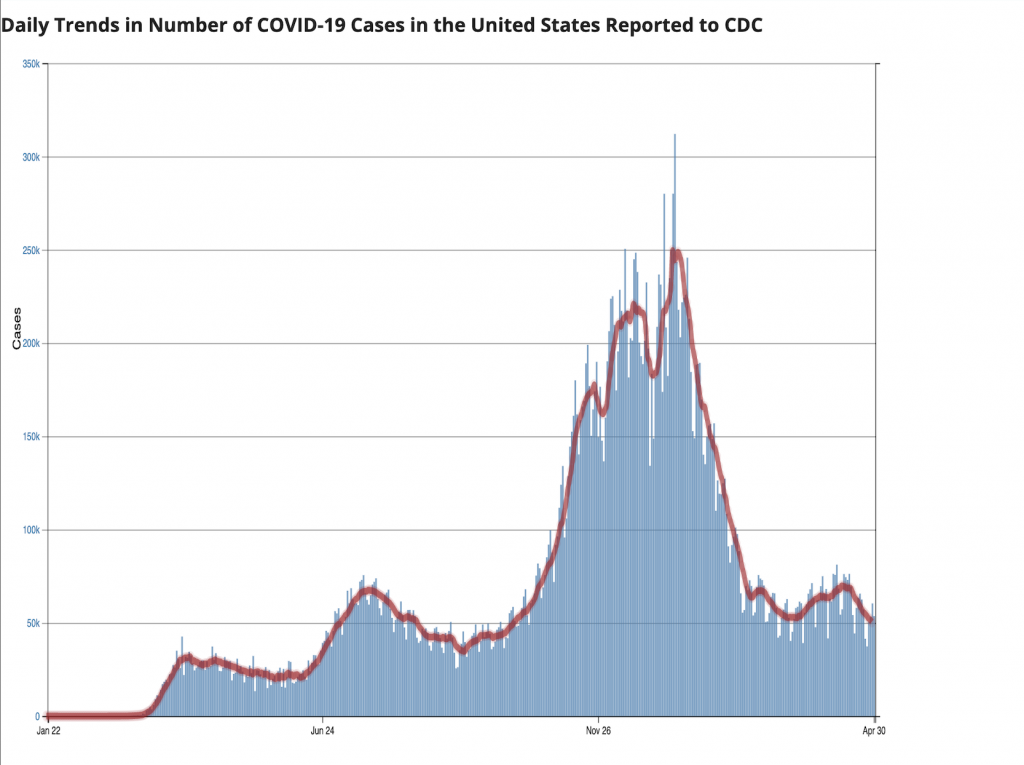

With the global vaccine rollout now underway, there are plenty of reasons to be optimistic about an economic rebound ahead. As lockdowns end, restrictions lift, and new COVID-19 cases continue on a downswing trend, the commercial real estate industry can certainly expect some relief as we enter into the “Next-Normal.”

The CDC COVID Data Tracker (below) tracks daily trends in the number of COVID-19 cases in the U.S. as reported to the CDC by state and territory. As the below Data Tracker illustrates, the COVID-19 surge trend appears to be behind us.

Source: CDC COVID Data Tracker

While we aren’t completely out of the woods yet, things are looking up for industry recovery. And although we still have many unanswered questions, we also now have the forward momentum we lacked for so long, which allows for the big-picture planning needed for success in a post-pandemic world.

The global pandemic upended daily life for more than a year. It has changed how we live, where we work, even what we wear on our faces. As a result, we are seeing major shifts in consumer behavior, consumption, and lifestyle, among other things. Data collected during 2020 and currently in 2021 shows that several sectors of the commercial real industry are certainly still feeling the weight of these shifts.

Sectoral Impact

RETAIL

The Retail sector took a significant blow as the pandemic made nonessential in-person shopping quite literally illegal for a period. As Americans sheltered indoors, everyday activities such as going to the grocery store were now weighed under a contagion risk analysis. Consumption that would have normally been completed in-person has quickly flowed into online orders. The e-commerce share of retail consumption has steadily risen for more than two decades, reaching 11.8% in Q1 20201, but as the full effect of the lockdown reached a fever pitch in Q2, the share ballooned to 16.1%. While the share came down to 14.0% through Q4 2020, reflecting some natural reversion, the familiarity gained by consumers cannot be undone, and the pandemic has permanently accelerated some retail activity away from brick-and-mortar.

At the same time, manufacturers don’t have the same options they once did: As governments enacted state-wide lockdowns and shelter-in-place orders to limit the spread of COVID-19, manufacturers across the globe — which typically operate with long lead times — were brought to a complete halt. The manufacturing sub-sector has since been fighting an uphill battle, but as market conditions continue to improve, there is hope that factories will have the capacity to gain back some of the productions they lost in 2020.

INDUSTRIAL

For the Industrial sector, particularly warehouse spaces, there was a period in 2020 just ahead of the pandemic and the rapid shift to record levels of online shopping when rent growth for the overall Industrial sector was pacing ahead of cold storage. (A cold storage warehouse is used to store fresh and/or frozen perishable fruits or vegetables, or any combination thereof, at the desired temperature to maintain the quality of the product.) Cold storage rent growth has been rising since the start of the pandemic in 2020. Prior to the pandemic, rent for cold storage space averaged around $10 per square foot; currently, that number could vault to as much as $30 per square foot.2

As of February 2021, the Industrial sector has seen production drop by nearly 5%, compared to a year prior, while retail sales have increased by over 6%.3

HOSPITALITY

Hospitality was, and continues to be, among the hardest-hit industries during the pandemic. Some research suggests that recovery to pre-COVID-19 levels for the industry could take until 2023 or later. However, things already seem to be looking up for Hospitality: For the week ending March 13, 2021, U.S. hotel industry RevPAR was $53.45 — a decline of only 15.8% from the same week in 2020, which is mostly a function of easier comparisons, according to data from STR, CoStar’s hospitality analytics firm.4

Looking Ahead: The Road To Recovery

Economic recovery in a post-pandemic world depends on several factors. The economic impact of COVID-19 is being felt on a global scale, and with specific sectors more severely impacted, some may experience a quicker rebound than others once the crisis is behind us. Given the universal lifestyle changes people have had to make, and their subsequent effects on the economy, the COVID-19 crisis has pushed many industries to adjust rapidly… and continuously.

The recovery rate of various sectors will have a massive impact regionally over the next two years, according toa report by KPMG. And not all industries are equally affected: certain sectors of the economy will thrive once the pandemic is over, while others will face a seemingly endless headwind.

The Industrial sector seems poised for post-pandemic growth. A few sub-sectors are already beginning to see significant recovery:

Warehouses underlying e-commerce, such as cold storage space

Big-box retail selling essential goods, such as Walmart and Target

Office space in certain locations, such as suburban areas

In the long run, the Retail sector is likely to be the biggest casualty as we exit the pandemic. This sector was already struggling before COVID-19, with vacant suburban shopping malls and big retailers shuttering stores across the country. Since the pandemic hit, many well-known brands have all filed for bankruptcy. The weakness of the retailers themselves, the accelerated growth of e-commerce, and questions about how quickly shoppers will head back to the stores all weigh against a strong recovery.

If the laws of physics extend to commercial real estate, then 2021 should be a year of recovery in the Retail sector, especially as restrictions on density are further relaxed and the resumption of normalcy gains steam. Notwithstanding the short-term recovery, Retail remains in a period of secular reorganization, and the sector remains open to disruption for the foreseeable future.5

Like so many industries, Hospitality will also see both subtle and substantial shifts in the post-pandemic era. Oxford Economics reports that gross domestic product grew by 9% in the first quarter of 2021, which has positive implications for the American travel industry. Jan Freitag, National Director for Hospitality Analytics at CoStar, reported that the March 2021 revenue per available room percentage change was “very positive” at 34%.6

We are still far off from “normal,” though an accelerating vaccination rollout brings the promise of a more rapid return to normalcy. As the economy recovers, leaders in the commercial real estate industry must begin to turn their attention to preparing for opportunities presented in the post-pandemic world.

Seizing Our Opportunity

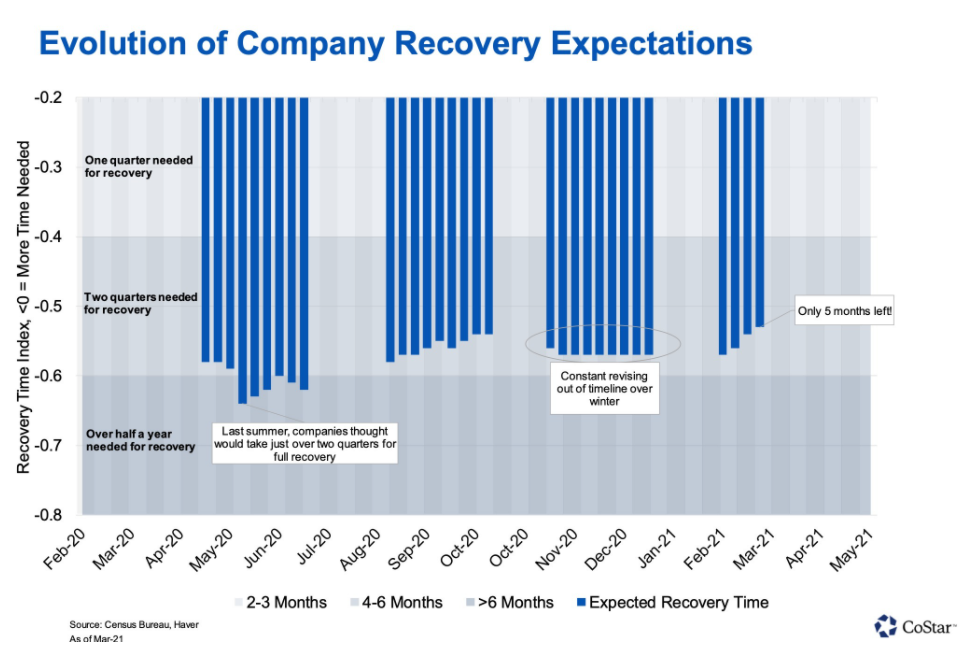

The Census Bureau’sSmall Business Pulse Survey(SBPS) measures the effect of changing business conditions during the COVID-19 pandemic on our nation’s small businesses. According to the SBPS, companies are consistently marking up when they expect conditions to normalize. As leaders in the industry, we now have clear opportunities to re-strategize asset attribution and ultimately redefine what post-pandemic success means for commercial real estate.

Source: CoStar7

Looking at history, other crises and external events show that generally,the CRE industry tends to lag the trajectory of the larger economy. But with the far-reaching effects of this pandemic, the CRE industry has felt the effects much earlier. In many ways, the pandemic has accelerated trends already occurring. While there is no specific answer or one-size-fits-all solution at this time, organizations that are able to move nimbly through the phases of recovery and embrace the “next normal” will thrive post-pandemic.

As the economy gains momentum, we will begin to see a split: organizations built to last, and those that are not. Those built to last, like SVN, are using this time to not only learn and emerge stronger, but also to prepare for and shape the future of commercial real estate.

Catalysts to Recovery: The SVN Difference

There are several components of SVN’s DNA working together to pull the future forward. For example:

A strong and established brand, foundation, and community backing Advisors, attracting new talent and supporting local independent ownership

Information & Fee Sharing: Every Monday, SVN Advisors present new and featured commercial real estate property listings on SVN | Live®. This live property broadcast is open to everyone in the industry.

Product Council meetings and collaboration tools for all asset classes such as Industrial, Office, Self Storage, and Healthcare

Online and scalable training to expand teams quickly, such as our SVN System for Growth courses and digital onboarding support

Advanced digital recruiting tools, such as Mike Lipsey’s System for Success online training for Advisors

Consultation support for asset attribution to establish team development

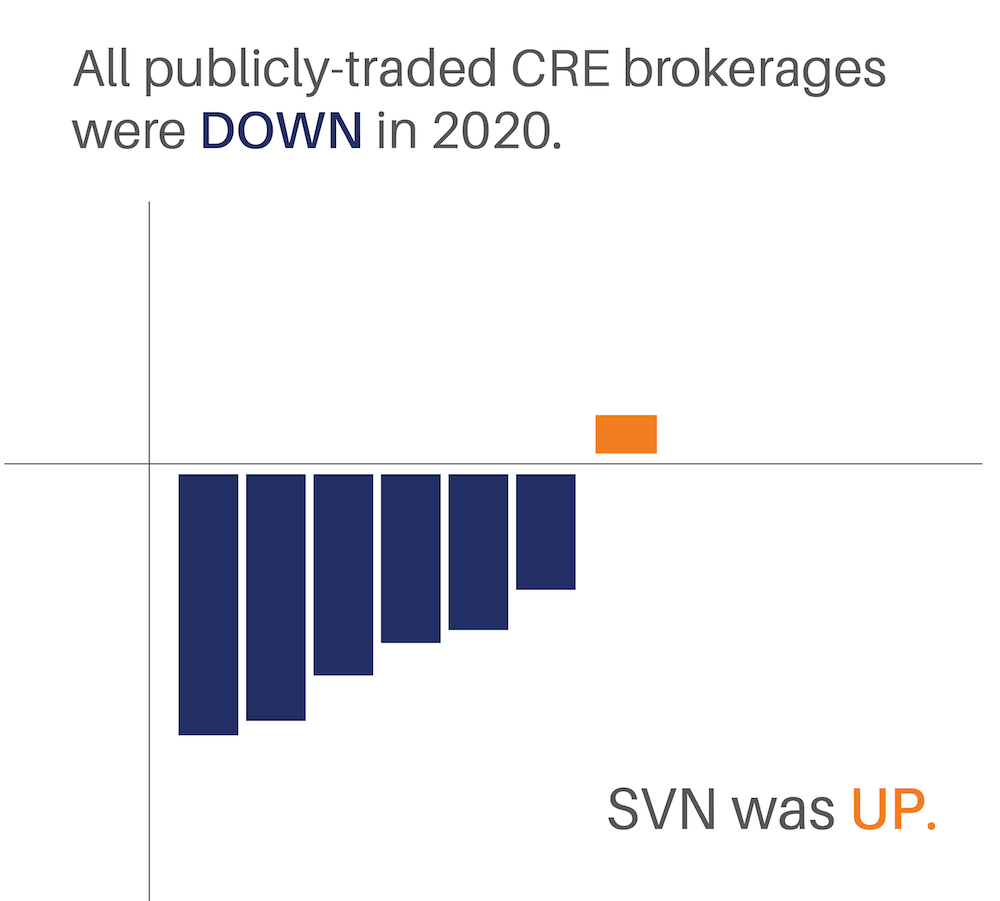

SVN was built to be future-proofed. That’s why, from 2019 through 2020, SVN’s gross commission income grew 3.1%… when everyone else was down. When all publicly traded CRE brokerages were up against double-digit declines — some facing 30% or more in lost revenue — SVN had its best year in company history. Models like SVN, which embrace automation, collaboration and cooperation, are uniquely positioned to take market share in this era of change, as client behaviors and expectations evolve.

The SVN brand offers something completely different from what any local, regional, or national firm is offering.This is the SVN Difference.And this difference is what ultimately creates 9.6% more value for our clients.

The Future Is Now

There is significant hope that 2021 will be a year of earnest recovery. As of the March WSJ Economic Forecasting Survey, on average, leading economists expect the US economy to grow by 6.0%. If reality ends up matching expectations, 2021 will mark the fastest annual growth since 1984.

SVN Advisors are leading the way into the “Next-Normal,” pulling the future forward, enacting change where and when it matters most.

CINCINNATI, OHIO (November 16, 2017) SVN Affordable | Levental Realty (SVN Affordable), one of the nation’s leading commercial real estate firms specializing in affordable housing, brokered over $350 million in Project Based Section 8 and Section 42 transactions throughout the United States in seven months.

“We commend SVN Affordable | Levental Realty for their continued commitment to providing industry-leading service and expertise in the market to establish SVN as a leader in this sector,” said Kevin Maggiacomo, President & CEO of SVN. “SVN’s Shared Value Network, centered on the philosophy that proactive collaboration with the global commercial real estate ensures maximum value for a property, provides our franchises with the essential tools to deliver exceptional client service and drive successful business results as evidence by these noteworthy transactions.”

The transactions brokered by SVN Affordable include affordable multifamily properties of varying sizes and diverse locations across the country.

“SVN Affordable is a nationally recognized leader in the niche market of Affordable Housing brokerage focusing solely on valuing, marketing and selling Project-Based Section 8 and Section 42 housing through our national platform and proprietary database. Our financial, regulatory and statutory expertise, paired with our strategic alliance of industry professionals, allows us to successfully identify a customized disposition strategy and transaction structure that ensures maximum value and minimal risk for our clients,” said Gene Levental, Managing Director of SVN Affordable. “Given the current economic environment, we are able to appropriately advise sellers to ensure they have the opportunity to capitalize on the current momentum in the market and maximize on an aggressive pricing strategy.”

SVN Affordable advised the seller on each of these transactions:

New Jersey Portfolio: Consisting of eight individual multifamily properties located throughout Central and Northern, NJ, totaling 1,202 units. Seven of the eight properties closed at $181.5 million. The eighth property is set to close in the first quarter of 2018, which will bring the total portfolio value to $213 million. All of these assets benefit from long-term project based HAP Contracts.

Rand Grove Village: A Project -Based Section 8 multifamily property consisting of 212 units in Cook County IL. This property sold for $35 million.

Circle Terrace Apartments: Consisting of 303 units, located in Landsdowne, MD. This Project-Based Section 8 development sold for $30.5 million.

Pequot Highlands: Located in Salem, MA, this 250-unit RAD conversion is covered by a long-term Project-Based Voucher Contract and sold for $26.65 million.

Park Vista: Built in 2001, this 212-unit Low Income Housing Tax Credit property located in Watauga, Texas sold for $17.75 million.

Roxbury Hills Apartments: Located at 140 Humboldt Avenue in Boston, MA, this 111-unit multifamily development sold for $15.1 million. The property is encumbered by Mass Housing Affordability restrictions in perpetuity.

Mark Apartments: A 52-unit, Project-Based Section 8 property located at 959 St. Marks in Crown Heights, Brooklyn, NY, sold for $12.85 million.

Baltimore Gardens & Cleveland Gardens: Consisting of two projects covered by separate HAP Contracts, totaling 201 units, this Las Vegas, NV development sold for $12.35 million and will be preserved using Low Income Housing Tax Credits.

Berkeley Terrace: A Project-Based Section 8 development located at 10 Berkeley Terrace in Irvington, NJ consisting of 153 units. The property sold for $12.25 million.

About SVN Affordable | Levental Realty

SVN Affordable |Levental Realty is an independently owned and operated SVN® office working exclusively on affordable housing transactions across the country with offices headquartered in Cincinnati, Ohio. The SVN organization, a globally recognized commercial real estate franchisor, is comprised of over 1,600 advisors and staff in more than 200 offices across the globe, and provides services to over 500 markets across the United States. SVN’s Core Values of transparency, cooperation and organized competition center on what is truly important for achieving organizational success and lasting value. SVN’s unique Shared Value Network® is just one of the many ways that SVN Advisors create amazing value with our clients, colleagues and communities. For more information, visit www.svn.com.

According to the Bureau of Labor Statistics, the national unemployment rate has fallen to 4.3% as of May 2017. Most economists would describe this state of unemployment as near “full employment” as historical data analyses show that the country rarely dips below 4% and never for that long. Yet, this near historically low unemployment has occurred less from overly robust hiring, but instead from a lack of qualified workers able to fill open positions. In fact, the BLS reported in May a modest +138,000 jobs added to the economy, a good but not great number. Perhaps more importantly, the jobs report showed no single sector reporting significant losses, which indicates that all are hiring or holding steady. In addition, the only sector to have shown persistent losses over the last year, Mining (which includes energy production and exploration), has even reversed itself and is posting significant gains over the last few months. Therefore, the jobs report truly only supports the conclusion of an ever growing, albeit slowly, economy.

ECONOMIC GROWTH HELD BACK BY LOW LABOR FORCE PARTICIPATION RATE

The challenge lies in the measured economic growth rate which was reported as 1.2% first quarter revised annualized GDP growth by the BEA. Normally, such low unemployment would be accompanied by much higher GDP growth, as in the +3% range, but the U.S. economy has struggled to get above 2% over the past several years. The answer to this problem may be that the low unemployment rate is a result of a low supply of qualified workers and not an excessive amount of job creation. The labor force participation rate, which is the percentage of those theoretically able to work and/or desiring to work, remains low at 62.7%. This measure peaked above 67% in the early 2000’s, and has fallen in-part due to the retiring baby boomers. But following the Great Recession it fell rapidly down, approximately 66%, to this 62-63% range where it still hovers today. Why people are not desiring to or actually working as they did ten years ago is the subject of study and speculation beyond today’s scope. What is becoming clearer with each monthly jobs report, is that it is holding back broader economic growth.

COMMERCIAL REAL ESTATE IS HOLDING ITS VALUE

The impact this will have on commercial real estate investments in 2017 and beyond is difficult to predict, but some insights are clear. First, some economists are forecasting a mild recession 12 to 24 months from now, based largely on historic macroeconomic cyclical activity. In the past, such low levels of unemployment were often followed by a mild recession within the same timeframe. However, recessions are typically triggered by excessive speculation, risk-taking, and usually hyper aggressive lending that pushes the economy too far. The data does not show any such excesses, especially in the use of leverage or aggressiveness of lenders. So, such predictions may not come true. Second, the labor shortage is being felt very strongly in the construction services and materials sectors. This means the cost to build new properties is rising faster than market rents and prices can justify. The net result is commercial real estate will probably hold its value just fine, and in fact, appreciate in areas where there is short supply. In conclusion, according to the data, we are probably closer to the middle of the cycle than the end.

FOUR MAJOR COMMERCIAL REAL ESTATE SECTORS EXPERIENCED POSITIVE RENT GROWTH

Now that all the 1Q17 real estate and economic data has been posted and analyzed, it appears as though 2017 year to date is holding steady. All four major sectors experienced positive rent growth in the first quarter according to Reis, Inc. as apartments were up 0.2%, office was up 0.4%, industrial was up 0.6%, and retail was up 0.4%. These growth rates are slower than similar first quarters in recent years, but they still represent growing market demand levels. According to data from the National Council of Real Estate Investment Fiduciaries Pricing, growth and appreciation slowed and the index was up 1.5% in 1Q17. CoStar, who’s equally-weighted national price index grew 4.8%. In regards to overall pricing performance smaller properties are dominating larger ones. The CoStar value-weighted index, which is dominated by larger properties, fell -2.8% over the same time period. This trend has been growing since the start of the year.

NEW SUPPLY REMAINS WELL BELOW RATES

Many of those who are reviewing the slowing pricing data and overall rate of effective rent growth are asking “is this a top?”. The best is answer is to wait to draw any conclusions. New supply of nearly all property types remains well below rates and some are even close to having an oversupply. As a result, sustained declines in real estate pricing or net operating incomes are highly unlikely at this point. The employment market, which historically drives demand for commercial real estate, is as healthy as it has ever looked. The Bureau of Labor Statistics reports an official unemployment rate of 4.4% which matches pre-2008 recession lows. Further, the “underemployment rate” (known as U-6, which includes marginally attached workers and part-time workers seeking full-time employment) has fallen to 8.6%, which is also close to pre-recession lows. Optimism by business leaders has resulted in increased hiring which, according to the Conference Board, grew to the highest level since 2004 as measured by its CEO Confidence score which reached 68 in the first quarter. This score is up from 65 which was the score at the end of the year. (Any reading above 50 indicates optimism.) The survey results of CEOs reveal there is a continued desire to hire in 2017, but finding qualified workers may be a challenge.

ECONOMY POISED FOR GROWTH

The first quarter, which objectively was slower than 2016 readings, may not be indicative of the rest of 2017 and beyond. Arguably, the election result and corresponding rise in stock prices and interest rates was not forecast in 2016. As a result, it is possible that investment activity and price growth of commercial real estate slowed in 1Q17 for no better reason than buyers paused to assess what would happen to the capital markets given the changing landscape. While the new administration has yet to offer clear policy guidance, the overall assessment of the economy is that it is still poised and positioned for growth as of May 2017. In fact, many economists who predicted first quarter GDP would be slow, (the first reading was 0.7% growth according to the Bureau of Economic Analysis), have also predicted a late surge that could bring annual GDP growth to 2.5% or higher. This is why stock prices, and especially REIT prices, have remained relatively steady for most of 2017. The overall market is still optimistic and there is no reason change that view for commercial real estate.

As the new administration crosses its 100-day mark, there is great uncertainty about what types of policies, ranging from health care, immigration, tax, and regulatory reform, exist. In fact, the celebrated “Trump Trade” has more or less stalled as of today, but the gains remain locked in place for the most part. The business and investment world has collectively reached a “now what” posture. Overall, recent measures of consumer and CEO confidence continue to rise as consumer confidence rose to 125.6 in March, up from the prior reading of 116.1, and CEO confidence rose from its prior reading of 65 to 68. The bulk of the country remains steady with the rise of optimism detected post November 2016, despite the uproar presented by the nightly evening news

Unemployment Rate Near Historic Low

Recent economic data has added additional uncertainty into the discussion. The most recent monthly report shows that only 98,000 jobs were added, a decrease from the previously reported numbers which were well above 200 thousand each month. However, the headline unemployment rate also fell to a near historic low of 4.5%, indicating an overall tight labor market. Inflation, as measured by the Consumer Price Index, also had its first negative reading of -0.3% in March after many successive reports of greater than 2% annualized inflation. The net result is less certainty that the Federal Reserve will raise rates in the near term or that aggressively over the next year. With long-term bond rates already down 20 to 30 basis points from recent highs, the potential for an “overheating” economy where inflation runs wild seems less likely as of today than it did three months ago.

3 Reasons Why Uncertainty Could Be Good News for CRE

There are three main reasons why this level of political and economic uncertainty can be very good news for the commercial real estate sector.

The market believes the uncertainty has a positive tilt. It’s more likely that we will unexpectedly receive good news rather than bad news (such as a surprise passage of a tax reform package that’s good for business).

There appears to be a lower probability of rapid interest rate increases, and consequently cap rate increases. This should boost the confidence for real estate investors looking to make acquisitions today.

The underlying fundamental demand for commercial real estate space, including apartments, continue to grow. Yardi reported the first increase in five months in average national multifamily rents with a gain of $6 per month to a rate of $1,312. As always, the likelihood of having a perfect world for commercial real estate is low given that interest rates are staying steady while rents and occupancies continue to rise. Right now this appears to be the condition for at least the near term.

Even though the future can be uncertain, real estate is set to outperform stocks and bonds in 2017. In the last month, REITs provided a total return of 6.03% while the S&P 500 index only returned 0.12%. In addition, REITs set a multi-year record for amount of capital raised in the first quarter of ’17. Historically, REIT performance serves as leading indicator of future returns to private real estate.

According to the most recent published reports by the Conference Board, CEO Confidence spiked a highly significant 15 points as of January and the Consumer Confidence Index sits at 114.8 as of February, making each measure sit at 6 year and 15 year highs respectively. Confidence at these levels, especially when true for both consumer and business segments, leads to increased levels of investment and spending, both critical for demand of real estate. To appreciate why confidence is so high, it is important to look at the underlying fundamentals of the macroeconomy in early 2017.

CONSUMERS CONTINUE TO DO WELL IN 2017

Job growth remains robust with multiple months of 200,000+ net new jobs, specifically 235,000 in February per the BLS, and a steady, low unemployment rate, presently 4.7%. This has led to continued wage growth and personal income growth, 0.4% in January alone. In addition, record high stock prices and growing home prices all add up to a (financially) happy household. Spending is up too with retail sales at a record high in the latest monthly reading and a 5.56% year over year growth rate as of January according to the Census Bureau. This has increased growth in manufactured goods order in the US, up 1.2% in January and up six out of the last seven months. In summary, the growing wave of positive news that began in the third quarter of 2016, appears to only have accelerated into the first quarter of 2017. Whether it’s due to raw macroeconomic fundamentals, or optimism following the election, the fact is, consumers are doing very well today.

The business sector still appears to be under investing, with only 0.04% growth in fixed investment in the 4Q2016 and there is a lot ground left to cover to get to full growth in the economy. If businesses invest more vigorously, as CEO confidence and stock market levels suggest could happen, GDP growth should easily exceed 2% and may even approach 3%. Despite all the recovery and improvement, the US economy only managed 1.6% growth in 2016. Regulatory rollback and reform is the one area of the new administration’s agenda most likely to advance in 2017, although not without controversy. These are the aspects President Trump can influence without needing Congressional approval, in many instances, and is more likely the most tangible, real, and immediate area that is causing the rise in business sector optimism. Even if there are small changes, the threat of sudden negative changes or complex new regulations is substantially reduced, such as the sudden change to the Department of Labor’s overtime compensation rules in 2016.

SMALLER DEALS AND OUTPERFORMING SECONDARY MARKETS TRENDS SET TO CONTINUE

A wide range of commercial real estate organizations have also begun intense lobbying on regulatory reforms due to the relaxed lending restrictions stemming from Dodd-Frank to energy use reporting provisions enacted by HUD in FHA multifamily lending. If these efforts are even somewhat successful, commercial property investors will have good reason to be optimistic. So far, commercial real estate has not yet felt the full impact of the Trump administration, rising stock prices and, even to some degree, long term interest rates. All evidence suggests that the commercial real estate industry is equally, if not more, optimistic than the general business community. CoStar, who issues monthly pricing indices for commercial real estate, reported that its value weighted index fell 0.9% in January, up 5.5% year over year, while its equally weighted index rose 1.4% that same month, up 7.5% year over year. The difference is due to the equally weighted index being more representative of secondary/tertiary markets and deals of smaller size. This trend of smaller deals and secondary markets outperforming core assets and primary markets looks highly likely to continue for 2017, especially if the confidence and optimism holds.

Commercial real estate markets have been generally growing in terms of pricing, rental rates, and occupancies since approximately 2011 and many market participants are beginning to openly wonder where the market is in the “cycle”.

Since the topic of market cycles can be somewhat misunderstood, we want to offer some clarification before presenting our assessment. Some investors believe that markets experience cycles based on some uniform period of time; such as every “X” years. In reality, markets, such as those for commercial real estate, move from peaks to valleys based on changes in supply and demand and any observation of timing is purely coincidental. An asset will see a “peak” and then decline when supply exceeds demand and this is when investors should look at changes in fundamentals to determine the relative risks and rewards of their investment due to cyclical forces.

CRE Markets Remain Healthy in Early 2017

With data available through the end of 2016, it is easy to see that most commercial real estate asset types are in the middle of the expansion phase of the real estate cycle. These are periods of long term growth in rents and declines in vacancy. According to REIS, all four major real estate classes experienced rent growth in 2016; 3.6% for apartment, 2.0% for retail, 2.4% for office and 2.2% for industrial. Office and industrial markets are experiencing the most absorption and improvements in occupancies and thus appear “earliest” in the expansion phase with year-end vacancy rates of 15.8% and 10% respectively. Retail vacancy rates remained flat at 9.9%, which given the number of “big box” closures, is actually impressive and masks the reality that many retail properties are actually experiencing rental rate growth and near full occupancies. The apartment sector, which began 2016 as the most watched sector given its 1.8% increase in supply, ended at 4.2% vacancy which is unchanged from 2015. Early 2017 data from Yardi Matrix shows modest rent growth has resumed which when considered with the rate of job creation, actually suggests that the apartment sector is not anywhere near as oversupplied as some have feared. However, relatively speaking, it is certainly the “latest” in the expansion phase. Overall, in early 2017 the fundamentals of commercial real estate markets still appear to be relatively healthy. In addition, given the current growth and optimism in the economy, they have room left to run in most situations.

2016 Transaction Volume is 3rd for Highest Recorded CRE Sales Activity

Prices of commercial real estate are a result of interactions between space markets (supply and demand) and the capital markets (competition for investment dollars). According to Moody’s and Real Capital Analytics, commercial real estate prices grew 9% in 2016 for another record breaking year. However, transaction volume was down 11% in 2016, but the year still ranks third after 2015 and 2007 for highest recorded commercial real estate sales activity. Overall, increases in interest rates and the 2016 decline in sales volume suggest the capital markets may put less pressure on price growth in 2017 than in recent years. The question of what cap rates will do given recent rate rises remains open but early evidence suggests that spreads are compressing and cap rates have shown minimal increases, however, this is still “too early” to call.

As of mid-February 2017, the commercial real estate markets appear to remain in expansion mode and 2016 was by all measures, a great year. If growth sustains, as the stock market is suggesting with its setting of new record highs every so often, fundamentals of commercial real estate should keep on moving upward as well. Census Bureau data showed that 2016 was a year for growth in construction spending; up 7.8% for nonresidential (commercial) and up 4.5% for residential (includes apartments). Therefore, there is more new supply coming but all the data suggests there is more than sufficient demand to keep the market in balance and growing.

Mortgage Rates Rise as Lenders React to Market Pressures

In response to a growing economy and inflation pressures, the bond markets, and now the Federal Reserve, appear positioned to support higher short term and long term interest rates. In a move that had been long anticipated, the Fed moved the target for the Fed Rates up 25 basis points from 0.5% to 0.75 % in December. It is expected that the Fed Rates could move two to three times more in 2017 depending on the rate of growth experienced this year. Prior to the Fed decision, long term bond rates moved in reaction to the election, with the 10-Year Treasury going form a three-month low of 1.74% to a three-month high of 2.60% in less than a month. Bond rates have since settled back below 2.40% as of January 17, 2017. This move represented a lot of pent up desire to sell bonds and buy stocks. Early indications are that mortgage rates, both residential and commercial, have moved in similar fashion as lenders quickly react to market pressures. This dynamic is likely to continue for much of 2017. If you invest in commercial real estate, here is how to adjust.

Future Growth in Economy, Jobs Could Increase Demand for Commercial Real Estate

First, realize that these moves in interest rates are related to the anticipation of good news, specifically, about the macro economy and to some extent stock prices. GDP has been reported to have grown at 3.5% in the 3rd quarter of 2016 before any potential “Trump” effect could be measured. Job growth has mostly sustained at robust, consistent levels as unemployment sits at near full employment at 4.7%. Of course, the biggest impact has been stock equity prices. The S&P 500 and Dow Jones Industrial Average have risen approximately 10% since the election as a result of anticipated future growth. This future growth in the economy and jobs, if it materializes, will also mean increased demand for all types of commercial real estate, resulting in a possible rise of rental rates and occupancies.

Second, interest rates, assuming they continue to rise, are still far below long term averages. For historical reference, the yield on the 10-Year Treasury averaged 3.58% from 2001 through 2015, and they were much higher in the fifteen years prior. Through this same period of time leveraged private real estate averaged an annual total return of 13.71%, according to the Lakemont Group (analyzing NCREIF return data), beating the average annual return on REITs, 13.19%. Therefore, real estate has and can continue to perform well in higher rate environments.

Finally, rising rate environments require different management strategies than flat or falling rate environments. As inflation is the natural companion of rising interest rates, the ability to push rents upward over time should, in theory, be easier. Flat long term leases are not as advantageous, and will not create as much value on a relative basis. In general, the more realistic upside potential a property’s rent roll presents, the more it could be worth. On the other hand, expenses are likely to rise at a faster rate. Therefore, lease structures that pass expenses, or at least their annual growth, on to the tenant will result in better cash flow and higher valuations. There is also the issue of borrowing in a rising rate environment. For long term holds the answer seems simple – fix long term rates. In reality, it’s much more complex, as accepting a variable rate will result in the greatest present day savings, but with more long term risk. The spread between variable and fixed rates historically gets much wider when lenders expect rates to rise in the near and long term future. As counterintuitive as it sounds, it may actually be more prudent to borrow at variable rates today than before. As long as the property can grow rents and the tenants can absorb increases in expenses, cash flows may be higher, even for the long term.

The retail real estate market, having long been the most segmented and divided sector of commercial real estate, was the most uniquely impacted in the last downturn and recovery. Grocery anchored neighborhood centers and free standing national credit retail properties have performed exceedingly well while regional malls, power centers, and non-anchored neighborhood strip centers have lagged in terms of price and rents. The slow economic recovery and ever growing share of e-commerce has made investment in retail real estate less desirable to sectors like multifamily and office. However, with this trend most likely changing in the next few years, retail may be one of the best investment opportunities for 2017. Here are three reasons this could be the case.

First, the economy may have now turned the corner and reentered a faster growth phase. GDP was last estimated to be growing at an annualized rate of 3.2% and unemployment has fallen to 4.6%. Retail sales continues to set new all-time records almost every month with annualized growth rates routinely near 3% according to the Census Bureau. As more people work due to the growing economy, they will have more money to spend. In fact, measures of consumer confidence, median household income, and total personal income have all shown strong growth and improvement in the last several months causing some to forecast yet another record breaking year for holiday sales. Regardless of online shopping, people are spending more at all types of retail establishments. Given that there has been a relatively low rate of new retail construction, it is almost unavoidable for retail rents and occupancies to rise resulting in the rising profitability of retail real estate investors. This rate of rent and occupancy growth may be the fastest of all property sectors in 2017 (at least for some markets).

Second, the retail landscape appears better equipped to compete in the new “digital” sales marketplace. Traditional retail tenants are now embracing an “omnichannel” approach, meaning dual focus on in-store and online sales, and recent research by the International Council of Shopping Centers (ICSC) indicates it is starting to show success. According to ICSC, 80% of Black Friday/Thanksgiving weekend shoppers made purchases at physical stores and 28% of those who purchased goods online opted to pick up the orders at a physical store (i.e. “site-to-store”) where 64% of those shopper made additional in-store purchases. Thus, the view that a store can be “online only” appears to be diminishing. In fact, even online giant Amazon is now actively seeking to open physical stores to facilitate order pick-up and enhance impulse purchases. In short, the storefront is not “dead”, just redesigned. Additionally, some categories such as home improvement, furniture, and restaurants cannot be easily moved online. All of these sectors are showing growth in sales and even store openings.

Third, many retail properties are located on great pieces of real estate in premier locations. There remain potential shortages for all types of commercial real estate including office, self-storage, heath care, and even apartments in many markets and sub-markets across the country. Retail sites are potentially the best redevelopment and repurposing sites in many in-fill markets. Retail can be converted to office/health care uses with very little costs; even self-storage is feasible for large vacant anchor spaces. Meanwhile, getting new sites approved for development is taking longer and costing more in many, if not most markets and, as municipalities seek to “beautify” older properties the redevelopment of existing buildings is getting relatively easier. Therefore, many retail sites, which are typically relatively low intensity uses, are actually easier to build on than raw, un-entitled land.

With an in-depth understanding of the local market, an investor can purchase a substantial income stream today with a potentially great exit strategy in the future. The key is creative vision and a good understanding of the micro forces in the sub-market (think location, location, location).

BEA reports 3Q2016 GDP growth is highest in 2 years.

From the shadows cast by the Presidential Election earlier this month, the Bureau of Economic Analysis (BEA) released a big “surprise” during the end of October. However, coverage of this news was relegated to the back page due to the election. That news was reporting that the first estimate of third quarter GDP growth came in at an annualized rate of 2.9%, the highest reading in two years (full report). Following the election, stock markets rallied to set new all-time highs and interest rates spiked considerably, with the 10-year treasury moving from 1.82% to 2.32%, a 27% increase. While much of the election’s impact on markets has since been discussed, the underlying status of potential growth (irrespective of the outcome of the election) is probably the bigger story.

While first estimates by the BEA are notoriously prone to error and likely to be revised, quarterly financial results of many publicly traded companies seem to be equally aligned as are recent readings of consumer health and sentiment. So for the time being, the market expects the US economy to grow at a more robust pace than the “slow” sub 2% expectations held just a month ago. For commercial real estate investors this is not new news. Rents and occupancies have been growing for years, but the reality of operating in a rising interest rate environment is a new phenomenon. Assuming the present situation holds, it is rational to expect treasury rates and bank lending rates to drift upwards, occasionally in big steps for much of 2017. This should not cause any great calamity, but upward movements in cap rates should be expected in some markets and asset classes. Losses from cap rate reversion will be offset, at least partially, by continued growth in net operating incomes. However, this is more of a long term effect.

Recent third quarter results from multiple real estate data providers, including REIS, CoStar, and NCREIF, were all positive with some slowing in the rate of appreciation and rental rate growth. If these growth expectations hold, it is quite possible for 2017, and even possibly in 4th fourth quarter 2016, to show that we will experience much faster growth. There is some evidence that the election and its uncertainty was holding back economic growth in 2016 more than previously thought. With this uncertainty gone, and with initial first impressions that a Trump presidency will be pro-growth, it is possible that pent up demand may be released. Still, the transition will not be complete until January, and even then it will take time to see what policy changes and enactments will actually transpire. Thus, cautious optimism is all that can be warranted today. Currently, the stock markets are firmly in this mindset, with growth expectations overpowering fear.

The specific impact by the Trump administration on commercial real estate remains to be seen. Infrastructure spending, tax cuts, and regulatory roll backs all portend signify positive results. Of course, an unpredicted increase in inflation and higher interest rates could mollify these impacts if too unbalanced. Although rents have paced ahead of overall inflation for the past several years, by nature, this trend should reverse itself over time. So celebrate the New Year as most expectations looks positive for the near future following the election, but be wary of too much of a good thing.

What Makes SVN® Different

Please provide us with your details below to download our value proposition.

Contact SVN®

Please can you provide us with the following details so a member of our team can contact you.

CINCINNATI, OHIO (November 16, 2017) SVN Affordable | Levental Realty (SVN Affordable), one of the nation’s leading commercial real estate firms specializing in affordable housing, brokered over $350 million in Project Based Section 8 and Section 42 transactions throughout the United States in seven months.

CINCINNATI, OHIO (November 16, 2017) SVN Affordable | Levental Realty (SVN Affordable), one of the nation’s leading commercial real estate firms specializing in affordable housing, brokered over $350 million in Project Based Section 8 and Section 42 transactions throughout the United States in seven months. economists would describe this state of unemployment as near “full employment” as historical data analyses show that the country rarely dips below 4% and never for that long. Yet, this near historically low unemployment has occurred less from overly robust hiring, but instead from a lack of qualified workers able to fill open positions. In fact, the BLS reported in May a modest +138,000 jobs added to the economy, a good but not great number. Perhaps more importantly, the jobs report showed no single sector reporting significant losses, which indicates that all are hiring or holding steady. In addition, the only sector to have shown persistent losses over the last year, Mining (which includes energy production and exploration), has even reversed itself and is posting significant gains over the last few months. Therefore, the jobs report truly only supports the conclusion of an ever growing, albeit slowly, economy.

economists would describe this state of unemployment as near “full employment” as historical data analyses show that the country rarely dips below 4% and never for that long. Yet, this near historically low unemployment has occurred less from overly robust hiring, but instead from a lack of qualified workers able to fill open positions. In fact, the BLS reported in May a modest +138,000 jobs added to the economy, a good but not great number. Perhaps more importantly, the jobs report showed no single sector reporting significant losses, which indicates that all are hiring or holding steady. In addition, the only sector to have shown persistent losses over the last year, Mining (which includes energy production and exploration), has even reversed itself and is posting significant gains over the last few months. Therefore, the jobs report truly only supports the conclusion of an ever growing, albeit slowly, economy. macroeconomic cyclical activity. In the past, such low levels of unemployment were often followed by a mild recession within the same timeframe. However, recessions are typically triggered by excessive speculation, risk-taking, and usually hyper aggressive lending that pushes the economy too far. The data does not show any such excesses, especially in the use of leverage or aggressiveness of lenders. So, such predictions may not come true. Second, the labor shortage is being felt very strongly in the construction services and materials sectors. This means the cost to build new properties is rising faster than market rents and prices can justify. The net result is commercial real estate will probably hold its value just fine, and in fact, appreciate in areas where there is short supply. In conclusion, according to the data, we are probably closer to the middle of the cycle than the end.

macroeconomic cyclical activity. In the past, such low levels of unemployment were often followed by a mild recession within the same timeframe. However, recessions are typically triggered by excessive speculation, risk-taking, and usually hyper aggressive lending that pushes the economy too far. The data does not show any such excesses, especially in the use of leverage or aggressiveness of lenders. So, such predictions may not come true. Second, the labor shortage is being felt very strongly in the construction services and materials sectors. This means the cost to build new properties is rising faster than market rents and prices can justify. The net result is commercial real estate will probably hold its value just fine, and in fact, appreciate in areas where there is short supply. In conclusion, according to the data, we are probably closer to the middle of the cycle than the end.

effect could be measured. Job growth has mostly sustained at robust, consistent levels as unemployment sits at near full employment at 4.7%. Of course, the biggest impact has been stock equity prices. The S&P 500 and Dow Jones Industrial Average have risen approximately 10% since the election as a result of anticipated future growth. This future growth in the economy and jobs, if it materializes, will also mean increased demand for all types of commercial real estate, resulting in a possible rise of rental rates and occupancies.

effect could be measured. Job growth has mostly sustained at robust, consistent levels as unemployment sits at near full employment at 4.7%. Of course, the biggest impact has been stock equity prices. The S&P 500 and Dow Jones Industrial Average have risen approximately 10% since the election as a result of anticipated future growth. This future growth in the economy and jobs, if it materializes, will also mean increased demand for all types of commercial real estate, resulting in a possible rise of rental rates and occupancies.